Economy

CBN threatens sanction over cash scarcity at ATMs

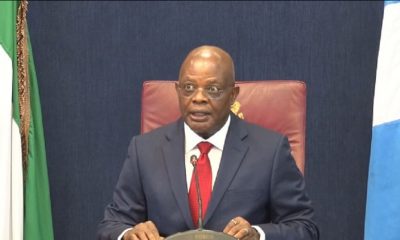

The Central Bank of Nigeria has threatened to impose fines on erring players in the financial sector over cash scarcity at Automated Teller Machines.

This announcement was made by the CBN Governor, Olayemi Cardoso, on Friday at the annual Bankers’ Dinner organised by the Chartered Institute of Bankers of Nigeria in Lagos.

There have been reports of cash scarcity at banks in recent times both at ATMs and over the counter in banks.

Cardoso stated, “We also recognise the ongoing challenges with cash availability at ATMs, which disproportionately affect ordinary Nigerians.

“To address this, we are conducting spot checks across the Deposit Money banks, and we impose penalties on the underperforming institutions. Effective December 1. 2024, customers are encouraged to report any difficulties with joint cash from bank branches or ATMs directly to the CBN through designated phone numbers and email addresses for their respective states.

“Guidelines will be distributed widely to raise public awareness. We will also urge full regulative compliance by all stakeholders, including mobile money operators and POS agents, to promote digital transaction channels and improve service delivery. I repeat, financial institutions found engaging in malpractices or sabotage will face changing penalties.

“The CBN will continue to maintain a robust cash offering to meet the country’s needs, particularly during high demand periods such as the festive season and year-end.”

The CBN governor also stated that so far, nearly N1tn has been recovered from development programmes.

Cardoso had announced the discontinuation of intervention programs at the 2023 Bankers Dinner and revealed that CBN pumped over N10tn into the economy through different initiatives in sectors ranging from agriculture, aviation, power, youth and many others.

He said, “As previously noted, the Central Bank’s return to orthodox monetary policy means that we will refrain from direct intervention in developmental initiatives. That said, I am pleased to report that as of October 2024, nearly N1tn has been recovered or repaid under previous development finance programs, thanks to the enhanced monitoring and enforcement of the guideline.

“Our focus remains on ensuring the effective utilization and recovery of outstanding loans within the framework of established guidelines. While development finance has a role in the economy of Nigerians, it must be approached with proper governance to achieve meaningful impacts.”

“On the outlook, Cardoso projected that with the improved framework for deploying products targeting the Nigerian diaspora and efforts to establish a well-founded FX market, “We anticipate increased diaspora and foreign investment over the next 12 months building on more resilient and liquid FX markets.”

He added that the apex bank has in its sight a monthly inflow of $1m in diaspora remittance.

“I recall when we took the view that it was important to focus on the diaspora remittances, and at that time, we said double. People thought it was an impossible thing to do, and it happened. As a result of that, we are even more happy to look at a target of $1m per month in the not-too-distant future,” he added.

Meanwhile, the CIBN conferred fellowship of the institute on the CBN governor and the governor of Lagos State, Babajide Sanwo-Olu.

Some dignitaries at the event include the Minister of Budget and Economic Planning of Nigeria, Atiku Bagudu, Chairman, the Senate Committee On Banking, Insurance and Other Financial Institutions, Senator Tokunbo Abiru, among others.

Oil prices plunged this week to $65 per barrel as the United States import tariffs and an unexpected OPEC+ supply hike erased $10 per barrel from global benchmarks.

The price appreciated last week when US President Donald Trump imposed tariffs on any country that buys crude from Venezuela.

However, oil prices turned around the corner as of Friday, with Brent falling to $65, the first time since 2021.

According to oilprice.com, the combined effect of Trump’s import tariffs, OPEC+’s inopportune decision to speed up the unwinding of production cuts, and China’s retaliatory actions wiped off $10 per barrel from global oil prices, “with ICE Brent falling below $65 per barrel for the first time since August 2021.”

The US West Texas Intermediate crude futures lost $4.96, or 7.4 per cent to end at $61.99.

“Seeing backwardation barely change compared to the beginning of the week, one could assume that US tariffs are the defining factor for the price change. Nevertheless, this week will not go down well in the history of oil markets,” oilprice.com reports.

China’s retaliatory tariffs on US goods have escalated a trade war that has led investors to price in a higher probability of recession.

China, the world’s top oil importer, announced it will impose additional tariffs of 34 per cent on all US goods from April 10.

According to Reuters, nations around the world have readied retaliation after Trump raised tariffs to their highest in more than a century.

Aside from the tariffs, another factor that further pressured oil prices was the Organisation of the Petroleum Exporting Countries and Allies’ decision to advance plans for output increases.

The group now aims to return 411,000 barrels per day to the market in May, up from the previously planned 135,000 bpd.

The Central Bank of Nigeria has injected $197.71m into the foreign exchange market on Friday, April 4, 2025, as part of its commitment to ensuring adequate liquidity and maintaining orderly market functioning.

This was disclosed in a statement on Saturday by the Director of the Financial Markets Department, Dr Omolara Omotunde-Duke, reiterating the bank’s stance on maintaining market integrity and operational transparency.

The statement read, “In line with its commitment to ensuring adequate liquidity and supporting orderly market functioning, the CBN facilitated market activity on Friday, April 4, 2025, with the provision of $197.71m through sales to authorised dealers. This measured step aligns with the bank’s broader objective of fostering a stable, transparent, and efficient foreign exchange market.”

The CBN said the intervention was in line with its broader objective of fostering a stable, transparent, and efficient foreign exchange market.

It added that it remained focused on sustaining liquidity levels to support smooth market operations amid ongoing global economic adjustments.

The apex bank said the decision to boost liquidity in the FX market came against the backdrop of significant shifts in the global macroeconomic landscape, which had affected many emerging markets and developing economies, including Nigeria.

It noted that the recent introduction of new import tariffs by the United States on goods from several economies had triggered adjustments across global markets.

It added that crude oil prices—a major revenue source for Nigeria—had dropped by over 12 per cent, settling at approximately $65.50 per barrel.

The CBN said the downturn posed challenges for oil-exporting countries, influencing exchange rate dynamics and market sentiment.

The CBN stressed that it would continue to monitor both global and domestic market conditions. It expressed confidence in the resilience of Nigeria’s foreign exchange framework, which it said was designed to adjust appropriately to changing economic fundamentals.

The bank also urged all authorised dealers to strictly adhere to the principles outlined in the Nigerian FX Market Code, promoting transparency and upholding the highest standards in their transactions with clients and market counterparties.

Meanwhile, Nigeria’s official exchange rate fell to N1,600/$1 at the end of trading on April 4, 2025, as the tariffs imposed during the Trump era continued to impact global markets.

Data from the CBN showed that the naira closed at N1,600/$1, marking a 1.9 per cent depreciation compared to the N1,569/$1 recorded the previous day.

The figure also marked the weakest level the naira had reached since December 4, 2024, when it closed at N1,608/$1. The exchange rate has now weakened by 3.9 per cent in the first four days of April, after closing March at N1,537/$1.

According to the CBN, the exchange rate closed at N1,600/$1 on Friday, marking a 1.9 per cent drop from the previous day.

The intra-day highs and lows were reported as N1,625 and N1,519 to the dollar, respectively. The intra-day high of N1,625 is also one of the highest levels recorded this year, indicating that traders priced the naira at significantly weaker levels.

Conversely, the intra-day low of N1,519/$1 suggests that some traders still priced the naira stronger, possibly betting on short-term interventions.

The NFEM rate, which represents the average exchange rate, closed at N1,567, the weakest the naira has traded this year and since December 4, 2024.

President Donald Trump has given TikTok a 75-day extension, staving off a ban on the Chinese-owned app just as its April 5 deadline loomed.

In a Friday post on Truth Social—his social media platform- the US President trumpeted an executive order to extend negotiations, a move he cast as a lifeline for a deal he’s keen to seal.

“My Administration has been working very hard on a Deal to SAVE TIKTOK, and we have made tremendous progress,” Trump wrote.

“The deal requires more work to ensure all necessary approvals are signed, which is why I am signing an Executive Order to keep TikTok up and running for

an additional 75 days.”

The ban, initially deferred on his first day back in office in January, had been barrelling toward an April 5 cutoff—now pushed out once more.

TikTok’s parent company, ByteDance, has been under pressure to divest its US business following bipartisan legislation passed in 2024 that mandates the app’s separation from Chinese ownership.

Trump laced his announcement with a jab at China, irked, he said, by his reciprocal tariffs. “We hope to continue working in good faith with China,” he added, calling tariffs “the most powerful economic tool” and vital for national security.

“We do not want TikTok to ‘go dark,’” he insisted, eyeing a resolution that keeps the app alive.

We look forward to working with TikTok and China to close the deal. Thank you for your attention to this matter!”

-

Politics12 hours ago

Politics12 hours agoTinubu Gives Fani Kayode, Others New Appointments (See Full List)

-

News12 hours ago

News12 hours agoDANGER! Ex-Soldier Abubakar Affan Vows to Kill VeryDarkMan ‘Like Deborah Samuel’

-

News15 hours ago

News15 hours agoWhy NYSC maybe extended by FG- Minister

-

News15 hours ago

News15 hours agoIbas moves to rehabilitate damaged Rivers LG secretariats

-

News12 hours ago

News12 hours agoJust in: Ex-Oyo governor, Olunloyo is dead

-

News15 hours ago

News15 hours agoWike commissions another solar-powered market in Abuja

-

Economy14 hours ago

Economy14 hours agoCrude prices slump to $65 first time since 2021

-

News7 hours ago

News7 hours agoHerdsmen Storm Benue Hometown Of Ex-Senate President David Mark